The Criminal Finances Act 2017 introduced two corporate offences: section 45 (failure to prevent the facilitation of UK tax evasion) and section 46 (failure to prevent the facilitation of foreign tax evasion).

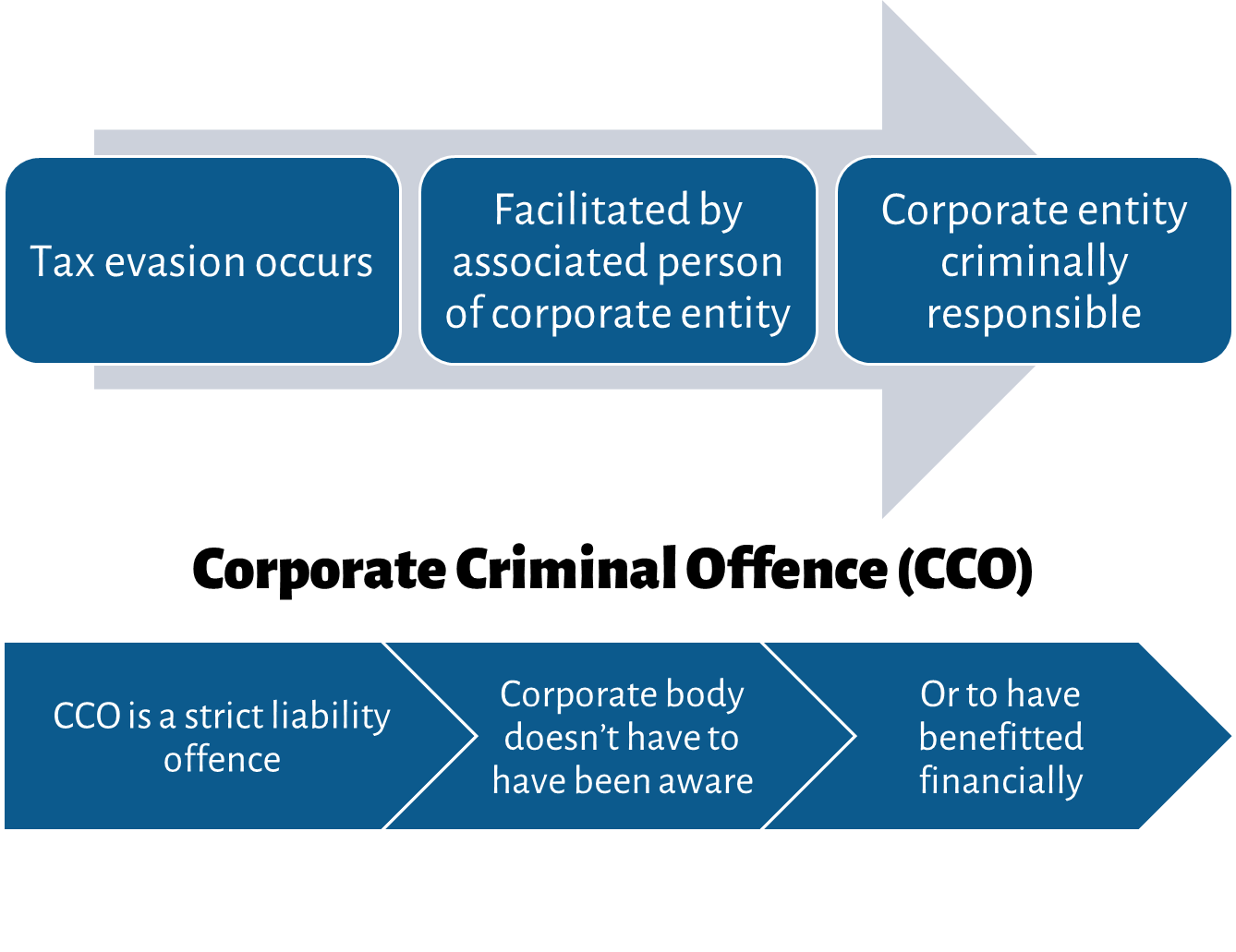

Where a taxpayer evades tax (stage 1) and an associated person of a relevant body (acting for or on its behalf) criminally facilitates that evasion (stage 2), the relevant body can be liable for failing to prevent it (stage 3).

The Corporate Criminal Offence (CCO) is a strict liability offence. A company or partnership does not need to have been aware of the facilitation, nor to have benefitted financially from the deliberate and dishonest behaviour.

An “associated person” isn’t limited to employees; it includes anyone performing services for or on behalf of the organisation (e.g., agents, contractors, certain intermediaries). You cannot subcontract your way out of CCO liability.

The only defence is to have “reasonable prevention procedures” (RPP) in place, or to show it was not reasonable to expect such procedures. HMRC groups RPP around six principles:

- Risk assessment.

- Proportionate, risk-based procedures.

- Top-level commitment.

- Due diligence.

- Communication (including training).

- Monitoring and review.

Due diligence is one of the principles to include in your reasonable prevention procedures (RPP). A relevant body should be using RPP to reduce the risk that associated persons criminally facilitate tax evasion (stage 2), and detect/respond to indicators of evasion risk in the supply chain. Ensure companies or individuals associated with you are not facilitating tax evasion (stage 2 offence).

Your organisation must (either directly or using other relevant bodies) apply due diligence when looking to employ the services of an individual or company to act on their behalf as part of the supply chain. Timely self-reporting and co-operation may be treated positively in charging decisions; on their own they do not establish reasonable prevention procedures.

Update: In August 2025 HMRC brought its first corporate prosecution under the CCO, underscoring the need to review and refresh RPP regularly.