End-hirers · Recruitment Agencies · Umbrellas · MSPs · Public Sector · OPRaaS Platform

April 2026 redrew the line between organisations that can show their compliance and organisations that hope it will hold. For board directors at end-hirers, recruitment agencies, umbrella companies, managed service providers (MSPs) and public-sector buyers, the shift produced something the old model never did: a compliance position you actually own, captured as dated, structured evidence and ready to hand over the moment a regulator, auditor or client asks. That record is compliance as an asset.

The mechanism is straightforward. HMRC’s Guidelines for Compliance 12 (GfC12) expect organisations to operate their own risk-based checks and retain their own evidence. The new Chapter 11 of the Income Tax (Earnings and Pensions) Act 2003 makes an umbrella’s unpaid PAYE recoverable from the recruitment agency or end-hirer. The Criminal Finances Act 2017 leaves “reasonable prevention procedures” as the only corporate defence available. Across all three, the organisations holding a dated, structured, audit-ready record are the ones placed to take the value. The rest carry the risk.

From badge collection to compliance as an asset

For years, the temporary labour supply chain ran on a model of comfortable distance. End-hirers maintained Preferred Supplier Lists, collected accreditation logos and circulated annual questionnaires. Agencies forwarded those questionnaires to umbrella partners and received self-declarations in return. The system produced documents, but not visibility, and not an evidence file any single party actually owned.

HMRC has now made explicit, in its updated Labour Supply Chain Assurance guidance (GfC12, January 2025), what reasonable looks like. Organisations are expected to operate their own risk-based checks and retain their own evidence. Industry accreditation and third-party assurance, on their own, are no longer sufficient. The compliance posture most organisations still operate has, in effect, been formally re-classified.

That sounds, on first hearing, like a warning. In practice it is the door opening on an opportunity. The moment HMRC tells the market what a defensible position looks like, the organisation that already holds that position holds something competitors cannot replicate overnight: an audited, repeatable, evidence-rich record of how the supply chain is run. The record is the asset. Compliance as an asset, in other words, is no longer rhetorical.

What April 2026 actually rewards

On 6 April 2026, Joint and Several Liability (JSL) came into force as Chapter 11 of Part 2 of the Income Tax (Earnings and Pensions) Act 2003. Where an umbrella in the supply chain fails to remit PAYE and Class 1 NICs, HMRC may now recover the unpaid amount from the recruitment agency that placed the worker, or, where the contract ran direct, from the end-client. There is no statutory defence.

Alongside JSL, the Criminal Finances Act 2017 continues to hold companies and partnerships liable for failing to prevent the facilitation of tax evasion by employees or associated persons. The only available defence is reasonable prevention procedures: a documented risk assessment, proportionate procedures, top-level commitment, communication, training and monitoring. The Economic Crime and Corporate Transparency Act 2023, in force from 1 September 2025, reinforces the same standard. Umbrella regulation, in force from April 2026, places formal legal responsibilities on the sector for the first time.

The common thread is straightforward. Each framework rewards the organisation that can produce, on request, an evidence file showing what it did, when, with whom, and what it found. Organisations that hold that file are credible, differentiated and trusted in the market. Organisations that cannot produce it are not.

The shift is binary. Compliance, captured daily, is the asset. Not the policy document. Not the badge on the website. The file.

Five outcomes a directed, evidenced framework gives you

A systemised, governed model, delivered through the OPRaaS LSCA 2.0 methodology, the OPRaaS Map, Train, Audit and Evidence platform and the OPRaaS Virtual Compliance Dashboard (OPRaaS VCD), produces five outcomes that ad-hoc compliance structurally cannot.

- Visibility across every tier. Agencies, sub-agencies, PEOs, umbrellas, CIS bureaux. The platform maps every intermediary and RAG-rates risk by route. There is no uncharted territory in the chain.

- Repeatable, timestamped evidence. A central repository of audit results, payslip samples, training completions, governance minutes and escalation logs builds one coherent narrative for HMRC, your auditor or your board, rather than a folder of PDFs to reconstruct under pressure.

- Early detection of high-risk patterns. Disguised remuneration, mini-umbrella fraud, phoenixism, CIS misclassification, SoW abuse. These patterns become detectable when the right questions are asked consistently. The framework asks them on your behalf.

- Proportionate, risk-based action. Scoring and red-flag outputs direct attention to the highest-risk nodes. Compliant suppliers are confirmed. Effort concentrates where exposure is real.

- Board and audit-committee confidence. The directed framework is the operating model boards and auditors increasingly expect to see for internal controls, and the standard major clients now write into contract.

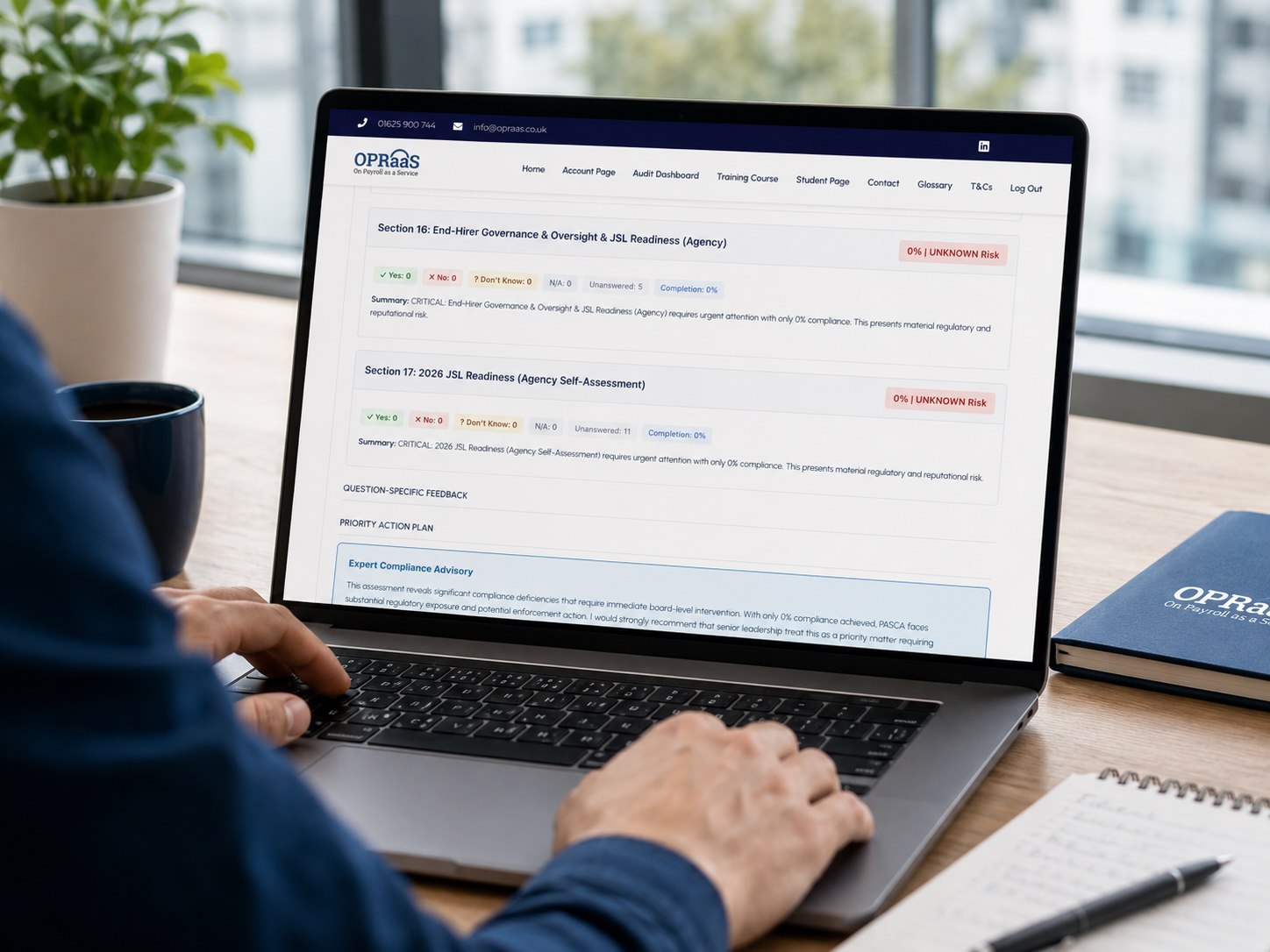

The OPRaaS VCD is what makes all five visible at a glance. It is the surface that turns daily compliance practice into a board-ready picture, and into the evidence file the moment someone asks for it.

For end-hirers: the defence file is procurement currency

End-hirers with material temporary labour spend used to be asked, “Are your agencies accredited?” The question now reaches further: “Can you show what you did, what you found, and what you changed?” That requires a named function with defined accountabilities, a live risk register, a training record for every relevant tier, and an evidence pack that can be handed over as one document.

The commercial dividend is real. End-hirers who can demonstrate a directed framework differentiate in procurement, in tender bids and in stakeholder reporting. They can tell boards and audit committees that contingent labour is governed, not just managed. In framework-led procurement, that is increasingly a competitive pre-condition as much as a credential.

For recruitment agencies: evidence is the differentiator

Agencies sit between two pressures. JSL flows up from the umbrellas they appoint, and evidence-led questions flow down from the end-clients who place workers through them. The agency that can produce a structured self-certification, an audit-ready evidence pack and training records for its own compliance team holds the PSL positions that less organised competitors lose. Compliance, properly directed, is no longer a cost line on the bid. It is the line that closes the deal.

For umbrella companies: governance is market position

Umbrella regulation places formal legal responsibilities on the sector for the first time. The well-governed umbrella, one that can demonstrate payroll accuracy, RTI compliance, correct deductions and the documented absence of non-compliant scheme features, is the one agencies will mandate and retain. On industry accounts, those without an evidence file are increasingly leaving PSLs as agencies tighten due diligence to control their own JSL position. The market is sorting itself by who can produce the file.

For public-sector procurement and SoW buyers

Public-sector framework agreements (RM6310 among them) and Statement of Works engagements have moved fastest in writing evidence requirements into contract. Buyers now expect a documented six-domain audit, structured evidence of the UK-law tests applied to each engagement, and live visibility into the supply chain throughout delivery, not at renewal. The directed approach produces all three by default, which is why it is the operating model OPRaaS recommends to any organisation bidding into framework or SoW work.

From compliance theatre to substance you own

There is a phrase that captures the model the market is leaving behind: compliance theatre. It produced documents and satisfied internal processes, but it would not, on OPRaaS’s reading, have survived an HMRC inquiry, because it was never designed to.

What replaces theatre is substance. A structured, digital, multi-tier, evidence-led framework that does not depend on hope, that assumes the question will be asked, and that builds the record accordingly. The HMRC standard, stated plainly in GfC12, is an organisation that can show structured checks, repeated over time, with evidence of what was found and what was done.

That is what OPRaaS is built to deliver. The methodology is OPRaaS LSCA 2.0. Its platform is OPRaaS Map, Train, Audit and Evidence. Its continuous oversight surface is the OPRaaS Virtual Compliance Dashboard. And the single output that matters when anyone asks, board, auditor, HMRC or end-client, is an evidence file that you own.

Where to start

If you are an end-hirer, an agency, an umbrella operator, an MSP, a public-sector buyer or an SoW compliance lead, and your current compliance position is not a single, owned file you can hand over today, that is where the work begins. Compliance as an asset is not a slogan; it is the operating discipline the OPRaaS team will help you stand up. Talk to OPRaaS about mapping your chain, directing the methodology, and standing up the OPRaaS VCD for your supply base.

Compliance is your asset. Evidenced, every day.

Drawing on HMRC’s Labour Supply Chain Assurance guidance (GfC12); the Finance Act 2025-26 provisions on Joint and Several Liability under Chapter 11 of the Income Tax (Earnings and Pensions) Act 2003; the Criminal Finances Act 2017; the Economic Crime and Corporate Transparency Act 2023; independent analysis by KPMG, RSM, Deloitte and Azets; and the OPRaaS LSCA 2.0 framework documentation.

Talk to OPRaaS about your supply chain.

Use the contact form in the sidebar to the right of this article, or email info@opraas.co.uk.

This article is published for general information and educational purposes only. It is believed to be accurate at the time of publication and reflects the legislation, HMRC guidance, and market practice referenced. It is not legal, tax, employment, accounting, or regulatory advice and should not be relied upon as such. Compliance obligations vary by organisation, supply chain, and engagement type; please consult your own qualified legal, tax, or compliance advisor before acting on any point covered here. Any images, screenshots, dashboards, or platform displays shown are for illustration and reference purposes only and do not necessarily depict the live OPRaaS platform, live customer data, or actual on-screen output. Trademarks, framework names, and statutory references remain the property of their respective owners. While we take every care, errors can occur; if you spot an inaccuracy, please let us know at info@opraas.co.uk.