RM6310 Lots 2 & 4 | RM6219 DPS | RM6237 DPS

OPRaaS established

Step methodology: map, train, audit, evidence

UK central government framework routes

Time-stamped evidence file, produced on demand

WHAT CHANGED FOR PUBLIC SECTOR END-HIRERS

Since 6 April 2026, new rules in the Finance Act 2026, amending Chapter 11, Part 2 of ITEPA 2003, let HMRC recover unpaid PAYE, NIC and the Apprenticeship Levy from other parties in umbrella supply chains, not just the umbrella itself. These are targeted umbrella-market measures, distinct from the older PAYE debt transfer powers.

HMRC’s GfC12 guidance expects organisations to run their own risk-based checks and keep an audit trail of what they did. Industry accreditations can be part of that picture, but on their own they are not treated as sufficient assurance. The standard has moved from holding a supplier list to demonstrating a governed, evidenced process.

HOW OPRaaS WORKS

We bring the rigour we apply across the UK labour supply chain to your public sector estate.

We map your supplier base across agencies, umbrellas and Statement of Work providers, so you can see your whole estate.

We train your finance, procurement and compliance teams to run the right checks and read the evidence with confidence.

We audit the controls you and your suppliers run, against the kinds of tests HMRC, tribunals and auditors apply in real cases.

We evidence the outcome in a single, time-stamped file the OPRaaS Virtual Compliance Director platform produces on demand, including risk heat-maps, exception reports and sampling results.

WHAT YOU GET WITH OPRaaS

OPRaaS turns regulatory exposure into a structured, audit-ready asset. Across your agencies, umbrellas and Statement of Work providers, you gain:

WHY IT MATTERS FOR PUBLIC BODIES

For public sector leaders accountable to Parliament, regulators and citizens, a governed supply chain protects four things at once.

Protect taxpayer funds from fraud, penalties and unplanned tax recovery.

Safeguard service continuity by keeping critical suppliers compliant.

Stay clear of National Audit Office, parliamentary and media scrutiny.

Ensure fair pay and prevent worker exploitation in your supply chain.

THE OPRaaS VIRTUAL COMPLIANCE DIRECTOR

Without hiring a new director-level board member, you gain a senior compliance function that runs the cycle and signs off the evidence, aligned to HMRC’s GfC12 guidance from pre-contract checks through to in-life monitoring. The OPRaaS Virtual Compliance Director (VCD):

Chairs your monthly governance calls, keeping suppliers, risks and actions on one agenda.

Runs the quarterly risk-check cycle on your supplier list: payslips, credit scores, director changes and VAT registration, via Companies House and Creditsafe.

Translates HMRC guidance into action so changes in the rules become tasks, not surprises.

Signs off the daily evidence file that gives your board, your auditors and HMRC a clear view of the checks you run.

APPROVED PROCUREMENT ROUTES

OPRaaS is available through the UK Government Commercial Agency, formerly Crown Commercial Service, giving public sector bodies compliant and efficient routes to procure our services.

Lot 2: External Audit, including PAYE, NIC, IR35 and CIS. Lot 4: Independent Assurance, including governance, ESG and controls.

Compliance training for procurement, HR, finance and operational teams, including workforce and Labour Supply Chain Assurance.

A cost-effective route for smaller LSCA consultancy and training engagements below relevant procurement thresholds.

Our methodology is trusted by councils, NHS Trusts and education bodies. Read more about LSCA compliance and solutions or explore the OPRaaS LSCA self-certification course.

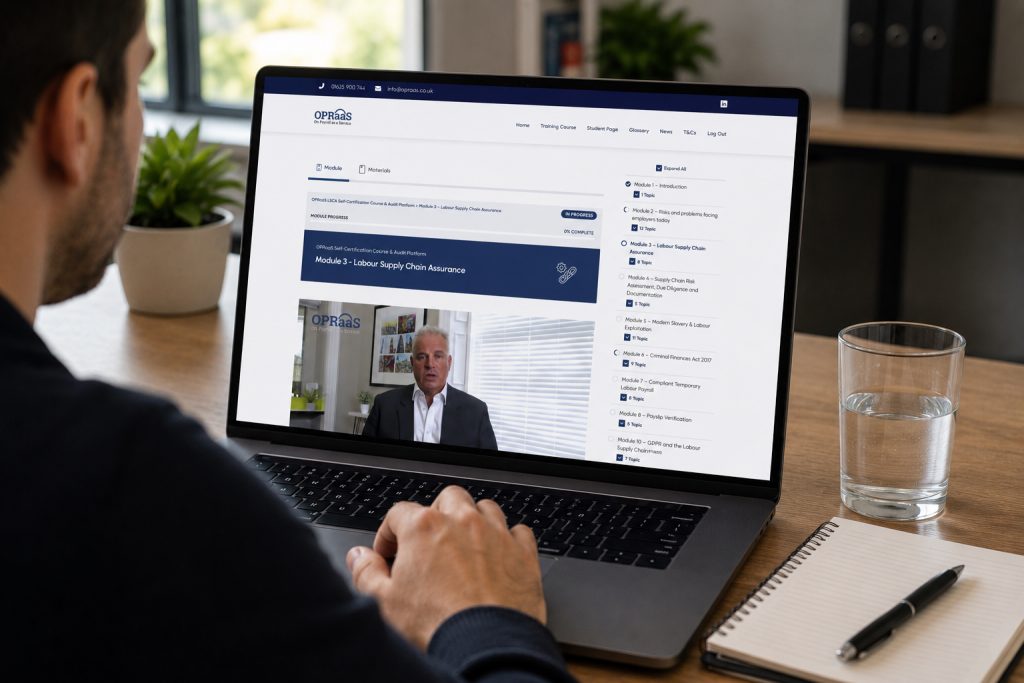

ONLINE LSCA TRAINING

Enrol your procurement, HR, finance and compliance teams on the OPRaaS LSCA self-certification course and audit platform, already trusted by councils, NHS Trusts and education bodies. The LSCA course builds the in-house capability your teams need to get the most from the Virtual Compliance Director service.

PUBLIC SECTOR VCD INFO PACK

A short, practical guide for public sector buyers: what changed under JSL, how the four-step OPRaaS method works, what the Virtual Compliance Director does, and the Government Commercial Agency routes to engage us.

Complete the short form and we will email a link to the PDF pack straight to your inbox.

LATEST INSIGHT

Recent OPRaaS analysis on labour supply chain assurance for public bodies.

PUBLIC SECTOR FAQS

Joint and Several Liability (JSL) came into force on 6 April 2026 under the Finance Act 2026 (Chapter 11, Part 2 ITEPA 2003). It is a new umbrella-market measure, distinct from the older PAYE debt transfer powers, that enables HMRC to recover unpaid PAYE and NIC from other parties in the labour supply chain where an umbrella has not met its obligations. In practice, public bodies are now expected to evidence the governance their agencies, umbrellas and Statement of Work providers run on their behalf, and to show how this aligns with HMRC’s GfC12 guidance.

Not on their own. HMRC’s GfC12 guidance expects you to run your own risk-based checks and keep an audit trail. Accreditations are a useful signal, but they must be tested and supplemented with your own evidence. The standard has moved from holding a supplier list to demonstrating a governed, evidenced process you can show on demand.

OPRaaS is approved on the UK Government Commercial Agency (formerly Crown Commercial Service): RM6310 Audit and Assurance Services Lots 2 and 4, RM6219 DPS and RM6237 DPS. That gives councils, NHS Trusts and central government a compliant, efficient route to engage us. See LSCA compliance and solutions.

The OPRaaS Virtual Compliance Director (VCD) is a named, retained governance function. It chairs your monthly governance calls, runs the quarterly risk-check cycle on your supplier list (payslips, credit scores, director changes and VAT registration, via Companies House and Creditsafe), translates HMRC guidance into action and signs off the daily evidence file your board, auditors and HMRC expect to see.

No. The point of the OPRaaS VCD is that you gain a senior compliance function that runs the cycle for you, without hiring a new director-level board member. We map, we train, we audit and we evidence, so your teams have a governed process rather than another spreadsheet to maintain.

A single, time-stamped evidence file the OPRaaS VCD platform produces on demand, covering the checks run across your supplier base and the references behind them. It is built to stand up to your internal audit team, the National Audit Office and HMRC.

No. This page and the Info Pack are provided for general information and do not constitute legal or tax advice. OPRaaS Virtual Compliance Director services are provided subject to terms and conditions of use; full details are available on request.

Comprehensive definitions for Labour Supply Chain Assurance compliance terminology

| Acronym | Full Term | Definition |

|---|---|---|

| CFA 2017 | Criminal Finances Act 2017 | UK legislation introducing Corporate Criminal Offence (sections 45/46): failure to prevent the facilitation of tax evasion. Requires businesses to implement 'reasonable prevention procedures' (RPP). The only defence is having adequate RPP or showing it was not reasonable to expect such procedures. |

| MSA 2015 | Modern Slavery Act 2015 | UK legislation mandating supply chain transparency and worker safeguarding. Section 54 requires commercial organisations with ≥£36m turnover to publish annual modern slavery statements (board-approved, signed by director, published on website with prominent homepage link). |

| IR35 | Off-Payroll Working Rules | Tax legislation determining whether a contractor should be treated as employed or self-employed for tax purposes. Since April 2021, medium and large private sector clients must determine contractor status and deduct employment taxes if inside IR35. Requires Status Determination Statement (SDS). |

| JSL | Joint & Several Liability | 2026 legislation imposing strict liability on agencies and end-hirers for umbrella company tax debts, even where due diligence checks have been undertaken. Makes supply chain participants jointly responsible for unpaid PAYE taxes. |

| AWR | Agency Workers Regulations 2010 | UK regulations giving agency workers the right to the same basic working and employment conditions as permanent employees after 12 weeks in a qualifying assignment (12-week parity rule). |

| Good Work Plan | Good Work Plan 2020 | UK employment law reforms requiring written 'section 1 statement' of employment particulars to be given to employees and workers on or before day 1 of engagement (effective 6 April 2020). Sets out key terms but is not itself the contract. |

| Construction Act | Housing Grants, Construction and Regeneration Act 1996 | UK legislation governing payment practices in construction contracts. Section 113 renders "pay when paid" clauses ineffective (except where upstream payer is insolvent). Requires clear due dates, final dates for payment, and compliant payment/pay less notices. |

| Pensions Act 2008 | Pensions Act 2008 | UK legislation establishing workplace pension auto-enrolment requirements. Employers must automatically enrol eligible workers into qualifying pension schemes and make minimum contributions. |

| Acronym | Full Term | Definition |

|---|---|---|

| HMRC | HM Revenue & Customs | UK government department responsible for tax collection, payment of tax credits and benefits, and enforcement of tax law. Operates PAYE, CIS, RTI systems and conducts compliance audits. Business Tax Account provides reconciliation data. |

| GLAA | Gangmasters and Labour Abuse Authority | UK government body regulating labour providers in certain sectors (agriculture, horticulture, shellfish gathering, food processing/packaging) and investigating worker exploitation. Operates licensing regime and has criminal investigation powers. Hotline: 0800 432 0804 (03000 718234 out of hours). |

| ICO | Information Commissioner's Office | UK independent authority upholding information rights. Enforces UK GDPR and Data Protection Act 2018. Personal data breaches must be reported to ICO within 72 hours where there's risk to individuals' rights. Provides guidance on lawful bases, DSARs, and data-sharing. |

| CITB | Construction Industry Training Board | Industry body that collects levy from construction employers (payroll ≥£80k in PAYE in last tax year, or ≥£80k net CIS payments) and provides training grants. CITB levy compliance is audited in construction-focused compliance audits. |

| Acronym | Full Term | Definition |

|---|---|---|

| PAYE | Pay As You Earn | HMRC's system for collecting Income Tax and National Insurance Contributions from employees' wages. Employers deduct tax before paying employees, then remit to HMRC. Operates under Real Time Information (RTI) reporting requirements. |

| CIS | Construction Industry Scheme | Tax deduction scheme for payments to subcontractors in construction industry. Contractors must verify subcontractors with HMRC before first payment and make deductions (20% for verified, 30% for unverified) on labour element only (excluding VAT and allowable materials). CIS300 returns due by 19th following tax month. |

| GPS | Gross Payment Status | CIS status allowing subcontractors to be paid without deductions. Must apply to HMRC and meet compliance tests (business test, turnover test, compliance test). Contractors must verify GPS and keep evidence; continue to file CIS300 but make no deduction. |

| CIS300 | CIS Monthly Return | HMRC return submitted by contractors detailing total payments made to each subcontractor and CIS tax deductions applied. Must be filed by the 19th following the tax month (6th–5th). Should reconcile to subcontractor statements and bank payments. |

| CIS340 | CIS340 Guidance | HMRC's official guidance document defining what constitutes 'construction operations' for CIS purposes. Only work qualifying under CIS340 can legitimately be paid through the Construction Industry Scheme. Includes site preparation, construction, alteration, repairs, demolition. |

| RTI | Real Time Information | HMRC system requiring employers to report PAYE information at or before each pay run. Consists of Full Payment Submission (FPS) for regular pay data and Employer Payment Summary (EPS) for adjustments/recoveries. Must reconcile to payslips and Business Tax Account. |

| FPS | Full Payment Submission | RTI submission reporting gross taxable pay, Income Tax, and NICs for each employee on each payday. FPS values must match payslips. Should not be used to mask under-deductions. |

| EPS | Employer Payment Summary | RTI submission used only for adjustments, such as recoveries, statutory payments, employment allowance claims, or apprenticeship levy. Should not be used to mask PAYE under-deductions. |

| Bacs | Bankers' Automated Clearing Services | UK electronic payment system used for direct debits and credits, including salary payments. Net pay on payslip must match Bacs transfer to worker's bank account. Never use "BACS" (incorrect). |

| UTR | Unique Taxpayer Reference | 10-digit number issued by HMRC to identify individuals and businesses for tax purposes. Required for CIS verification and self-assessment tax returns. Note: UTR alone isn't proof of CIS verification; contractor must verify with HMRC before first payment. |

| NIC / NICs | National Insurance Contributions | UK social security tax paid by employees (via PAYE), employers (as on-costs), and the self-employed (Class 2/4 via self-assessment). Funds state benefits including state pension, statutory sick pay, and maternity allowance. CIS deductions are payments on account of Income Tax and Class 4 NICs. |

| NMW | National Minimum Wage | Legal minimum hourly rate employers must pay workers in the UK. Rates vary by age band. Post-deduction pay (after deductions for employer's own use/benefit) must not fall below NMW. Records must be kept for 6 years. |

| NLW | National Living Wage | Higher rate of National Minimum Wage for workers aged 21 and over. Often referred to together as "NMW/NLW". Different from voluntary Real Living Wage calculated by Living Wage Foundation. |

| AE | Auto-Enrolment (Pensions) | Workplace pension scheme where employers must automatically enrol eligible workers (aged 22+ to state pension age, earning ≥£10k annually) into a qualifying pension. Minimum contributions, opt-out rights, and re-enrolment (every 3 years) required. |

| P45 | P45 (Leaving Employment) | HMRC form given to employees when they leave employment, showing pay and tax details for the year to date. New employer uses P45 to operate correct tax code. Emergency codes (e.g., 1257L W1/M1) apply without P45/P6. |

| Acronym | Full Term | Definition |

|---|---|---|

| DRC | Domestic Reverse Charge (VAT) | VAT mechanism for construction services where the customer accounts for VAT instead of the supplier. Applies to most construction services under CIS340. Designed to combat missing trader fraud in construction supply chains. |

| Kittel | Kittel Principle | EU/UK legal principle that a taxpayer who knew or should have known their transaction was connected to VAT fraud may be denied the right to deduct input VAT. Creates due diligence obligations for supply chain participants. |

| DR | Disguised Remuneration | Tax avoidance arrangements designed to pay individuals while avoiding income tax and NICs, often involving loans, offshore entities, or trusts. HMRC actively targets such schemes. Loan charge applies to outstanding loans. |

| Acronym | Full Term | Definition |

|---|---|---|

| SDC | Supervision, Direction or Control | Key factor in determining employment status under agency rules (ITEPA 2003 s44). If a worker is under supervision, direction or control by any person (client, agency, end-hirer) over how they work, PAYE must be operated. SDC alone is not the general CIS status test—apply usual status tests (control, substitution, mutuality). |

| MOO | Mutuality of Obligation | Employment status indicator examining whether the employer is obliged to provide work and the worker is obliged to accept it. Absence of MOO suggests self-employment; presence suggests employment. |

| SDS | Status Determination Statement | Document required under IR35 reforms (April 2021) where medium/large clients must provide written reasons for their determination of a contractor's employment status for tax purposes. Must be given before contract starts or worker begins work. |

| CEST | Check Employment Status for Tax | HMRC's online tool for determining whether a worker should be classified as employed or self-employed for tax purposes. Results are binding on HMRC if information provided is accurate and not relating to highly complex arrangements. |

| PSC | Personal Service Company | Limited company through which a contractor provides their services. Often used by contractors working outside IR35, but subject to IR35 rules if the underlying relationship is one of employment. Requires SDS from medium/large clients. |

| KID | Key Information Document | Plain-English factsheet (not a contract) that agencies must give to workers before they agree to an assignment (Conduct of Employment Agencies and Employment Businesses Regulations 2003). Includes worked pay illustration, deductions, who pays the worker, benefits. Must be updated within 5 working days of any change. |

| ITEPA 2003 | Income Tax (Earnings and Pensions) Act 2003 | UK tax legislation governing employment income. Section 44 contains agency rules requiring PAYE where worker is under SDC. Section 61N–61R cover off-payroll working (IR35) for public sector and (from 2021) medium/large private sector. |

| DBS | Disclosure and Barring Service | UK government service providing criminal record checks for employment purposes (particularly roles working with children or vulnerable adults). Processing DBS data requires DPA 2018 Schedule 1 condition and appropriate policy document. |

| Acronym | Full Term | Definition |

|---|---|---|

| Umbrella | Umbrella Company | Employment intermediary that employs agency workers and contractors. Handles PAYE, pension, and employment administration while the worker performs assignments for end-clients arranged through agencies. Employer NICs/apprenticeship levy must be funded from assignment rate, not charged to workers as deductions. |

| MUC | Mini Umbrella Company | Fraudulent scheme where multiple small umbrella companies are created to exploit employment allowances and avoid tax obligations. Often phoenixing after accumulating tax debt. A significant compliance risk that supply chain audits help detect. |

| Phoenix | Phoenix Company Scheme | Fraudulent practice where a company accumulates tax debts, is dissolved, and re-emerges as a new entity to escape liabilities. A key risk factor in supply chain due diligence. Tolerance of phoenix suppliers by end users enables fraud cycle. |

| Purported | Purported Umbrella Company | Entity presenting itself as a legitimate umbrella company but failing to meet compliance standards, potentially operating tax avoidance schemes or misclassifying workers. |

| Hybrid | Hybrid Payment Model | Pay arrangement combining different payment methods (e.g., PAYE + CIS, or PAYE + PSC). Requires careful status assessment to avoid disguised remuneration or employment status breaches. |

| Acronym | Full Term | Definition |

|---|---|---|

| UK GDPR | UK General Data Protection Regulation | UK data protection law (retained EU law post-Brexit) governing processing of personal data. Requires lawful basis (Art 6), data minimisation, security, transparency (Arts 13-14), and respect for data subject rights. Works alongside Data Protection Act 2018. |

| DPA 2018 | Data Protection Act 2018 | UK legislation supplementing UK GDPR. Schedule 1 sets conditions for processing special category data (health, biometric, union membership) and criminal offence data (e.g., DBS checks). Provides exemptions (crime prevention, tax collection, legal professional privilege). |

| DSAR | Data Subject Access Request | Individual's right under Art 15 UK GDPR to obtain copy of their personal data. Must respond within one month (extendable by 2 months for complex requests). Usually no fee. Must verify identity proportionately. |

| DPO | Data Protection Officer | Required role for public authorities or organisations conducting large-scale systematic monitoring or processing special category data (Art 37). Oversees data protection compliance, advises on DPIAs, and acts as contact point for ICO and data subjects. |

| LIA | Legitimate Interests Assessment | Assessment required when relying on legitimate interests (Art 6(1)(f)) as lawful basis. Three-part test: identify legitimate interest → demonstrate necessity → balancing test (interests vs individual rights). Appropriate for audit/assurance; avoid consent for audits. |

| DPIA | Data Protection Impact Assessment | Required assessment where processing is likely to result in high risk to individuals (Art 35). Must complete for large-scale, systematic monitoring or extensive special category data processing. Documents risks, mitigation measures, and necessity/proportionality. |

| RoPA | Records of Processing Activities | GDPR requirement (Art 30) documenting all personal data processing activities. Must include purposes, lawful bases, data categories, recipients, retention periods, security measures, and international transfers. Must be available to ICO on request. |

| IDTA | International Data Transfer Agreement | UK mechanism for lawfully transferring personal data outside the UK (replacing EU Standard Contractual Clauses post-Brexit). Required unless recipient country has adequacy decision or other derogation applies. Alternative: UK Addendum to EU SCCs. |

| SCCs | Standard Contractual Clauses | EU Commission-approved contract templates for international data transfers. For UK data exports, use UK Addendum to EU SCCs or UK IDTA. |

| Art 28 DPA | Article 28 Data Processing Agreement | Mandatory contract between controller and processor (Art 28 UK GDPR). Must cover: subject matter, duration, data types, processing instructions, confidentiality, security, sub-processors, data subject rights assistance, breach notification, data deletion/return, audit rights. |

| Art 26 | Article 26 (Joint Controllers) | UK GDPR provision for parties who jointly determine purposes and means of processing. Requires arrangement setting out respective responsibilities, data subject rights, and contact points. Different from controller-processor (Art 28) or controller-controller data-sharing. |

| Controller | Data Controller | Organisation that determines the purposes and means of processing personal data. Bears primary GDPR obligations. Agencies, umbrellas, and end-hirers usually act as independent controllers for their own audit/compliance purposes. |

| Acronym | Full Term | Definition |

|---|---|---|

| LSCA | Labour Supply Chain Assurance | Due diligence framework ensuring compliance with tax, employment, and ethical standards throughout the labour supply chain. Covers PAYE/CIS compliance, modern slavery, CFA 2017, worker rights, and IR35. Aims to detect exploitation, fraud, and phoenixism. |

| PSL | Preferred Supplier List | Vetted list of approved suppliers (typically umbrella companies or agencies) that meet compliance standards. Key governance control for managing supply chain risk. Should be reviewed regularly and require re-certification. |

| End-Hirer | End-Hirer / End Client | The organisation where agency or contract workers ultimately perform their work. Under current regulations, medium/large end-hirers have IR35 status determination responsibilities and supply chain due diligence obligations. |

| CCO | Corporate Criminal Offence | CFA 2017 offence: failure to prevent facilitation of tax evasion by an associated person. Three-stage liability: (1) taxpayer evades tax, (2) associated person criminally facilitates it, (3) organisation failed to prevent. Only defence: reasonable prevention procedures (RPP). |

| RPP | Reasonable Prevention Procedures | The only defence to Corporate Criminal Offence under CFA 2017. HMRC's six principles: risk assessment, proportionate procedures, top-level commitment, due diligence, communication (training), monitoring & review. Must be risk-based and documented. |

| SRO | Senior Responsible Owner | Senior person accountable for CFA 2017 compliance, risk assessments, and implementation of reasonable prevention procedures. Provides top-level commitment and board oversight. |

| MSAT | Modern Slavery Assessment Tool | UK Government tool (Home Office/Cabinet Office) for assessing modern slavery risks in supply chains. Free to organisations registered on UK Government Supplier Registration Service. |

| Acronym | Full Term | Definition |

|---|---|---|

| ASCA | Agency Self-Certification Audit | Most comprehensive audit form with 174 questions across 18 sections. Enables recruitment agencies to self-assess compliance with tax, employment, and supply chain obligations including PAYE, CIS, Modern Slavery, CFA 2017. |

| AUCIS | Agency Umbrella CIS Audit | Audit evaluating recruitment agencies' compliance with CIS requirements when engaging umbrella companies, ensuring proper tax treatment and supply chain integrity. |

| AUPAYE | Agency Umbrella PAYE Audit | Audit assessing recruitment agencies' oversight of umbrella companies' PAYE compliance, including tax deductions, National Insurance contributions, and payroll accuracy. |

| EHUCIS | End-Hirer Umbrella CIS Audit | Audit evaluating end-hirers' due diligence when engaging umbrella companies under CIS, ensuring supply chain compliance and proper contractor treatment. |

| EHUPAYE | End-Hirer Umbrella PAYE Audit | Audit assessing end-hirers' oversight of umbrella PAYE arrangements, covering payroll transparency and worker rights compliance. |

| EHSA | End-Hirer Self-Assessment Audit | Audit enabling end-hirers to self-assess their compliance with supply chain, tax, and employment obligations. |

| EHAA | End-Hirer Assurance Audit | Audit providing end-hirers with an independent assessment of their supply chain compliance, risk management, and due diligence practices. |

| UMBCIS | Umbrella CIS Audit | Audit evaluating umbrella companies' compliance with CIS requirements, including proper contractor treatment, tax deductions, and verification processes. |

| UMBPAYE | Umbrella PAYE Audit | Audit assessing umbrella companies' PAYE compliance, payroll integrity, and worker protection standards. Contains 21 sections (Section 1 info-only, Sections 2-20 audit, Section 21 declaration) vs 18 for most other audits. |

| Self-Cert | Self-Certification Audit | Generic term for labour supply chain compliance audits where organisations self-assess against tax, employment, and ethical standards. Provides documented evidence of due diligence for HMRC inspections. |

| Acronym | Full Term | Definition |

|---|---|---|

| Instance | Audit Form Instance | Individual audit submission. Users can create unlimited instances, each stored as WordPress custom post type with responses in wp_opraas_audit_responses table. Assigned to logged-in user via post_author field. |

| Completion | Completion Score | Frontend metric showing percentage of questions answered (any answer counts). Includes ALL sections: Section 1 checkbox, Section 2 (8 fields), Declaration (7 fields), and all audit questions. N/A responses count as answered. |

| Compliance | Compliance Score | Backend metric measuring quality of compliance. Scoring: Yes=5 points, No=0 points, N/A=0 points (excluded from maximum), Don't Know=1 point. EXCLUDES Sections 1, 2, and Declaration entirely. ≥80% = Compliant, 60-79% = Partially Compliant, <60% = Non-Compliant. |

| Evidence | Evidence Files | Supporting documents uploaded to substantiate audit responses. Stored in AWS S3 via WP Offload Media plugin, with Evidence Table providing S3-aware ZIP downloads that temporarily download from cloud before adding to archives. |

| Red Flags | Red Flags | Warning indicators in audit questions identifying practices that may indicate non-compliance, fraud risk (phoenixism, MUCs, disguised remuneration), or regulatory breaches requiring immediate attention and remediation. |